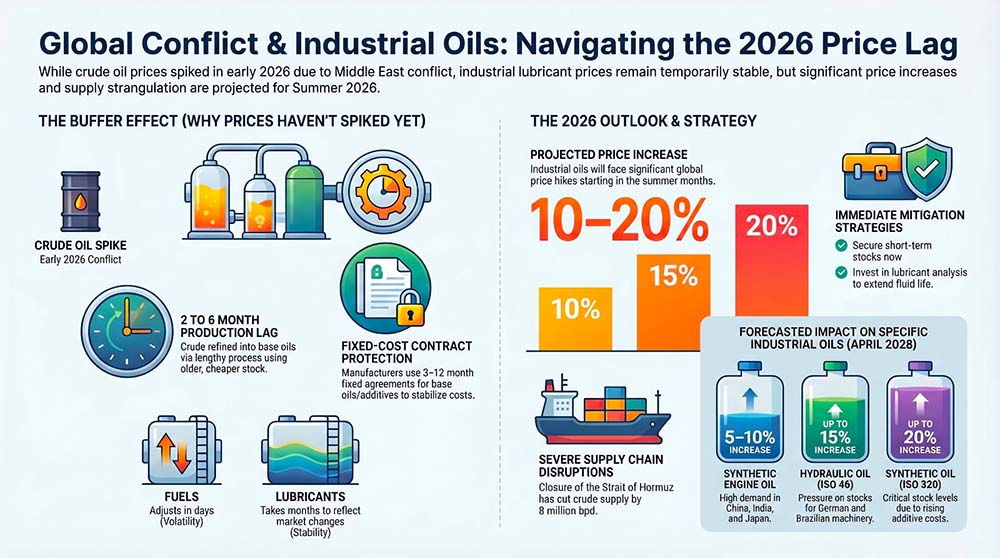

Crude oil prices have fluctuated significantly over the past 12 months, with a recent sharp increase in 2026 due to the crisis in the Middle East, while global lubricating oil prices remain relatively stable and do not directly track crude oil volatility.

An analysis of the monthly average crude oil prices (spot average of Brent, WTI, and Dubai in USD per barrel) and price estimates per liter for lubricants such as ISO 46 mineral hydraulic, engine synthetic, ISO 320 mineral and synthetic current shows that now there is no significant variation and depends more on brands and volumes.

| Month | Oil (USD/barrel) | Synth. Engine Oil (USD/L) | Hydraulic Oil ISO 46 (USD/L) | Mineral Oil ISO 320 (USD/L) | Synthetic Oil ISO 320 (USD/L) |

|---|---|---|---|---|---|

| April 2025 | 65.90 | ~10 | ~3 | ~4.8 | ~8 |

| March 2026 | 95.58 ▲ 45% | ~10 | ~3 | ~4.8 | ~8 |

Lubricants do not immediately reflect changes in oil due to long-term contracts and stocks.

Why is there no rise in lube oil prices if there was a rise in oil prices?

Lube oil prices have not risen immediately despite the recent increase in crude oil (from ~60 USD/barrel to 95 USD in March 2026) due to several structural factors in the industrial supply chain.

Main reasons

- Delay in the production chain: The oil is refined into base oils, a process that takes 2 to 6 months. Lubricants use stocks purchased at previous prices, cushioning rapid rises.

- Long-term contracts: Lubricant manufacturers sign fixed agreements (3 to 12 months) for base oils and additives, which represent between 70 and 80% of the final cost of the product, but are not adjusted daily like spot crude.

- Low proportion of crude oil: Only 50 to 70% of the lubricant is petroleum-derived base oil; the rest are imported additives (20-40%), packaging and margins, diluting the impact a little more, 10 to 20% of the final price.

- Isolated volatility: The oil base markets have their own dynamics (refinery supply, technical shutdowns, scheduled maintenance); they do not follow Brent/WTI 1:1.

- Stable demand and competition: Industrial, hydraulic, or gear lubricants, for example, are sold in large volumes with negotiated prices, without the “rocket-feather effect” as marked as in fuels.

Comparison with fuels

| Factor | Oil → Fuels | Oil → Lubricants |

|---|---|---|

| Time Adjustment | Days/weeks | Months |

| % Crude Oil in Cost | 50 – 60% | 50 – 70% (but fixed) |

| Market | Daily Spot | Contracts / Deferred Spot |

| Recent Example | Gasoline +18% in 1 week | Stable at 3 – 10 USD/L |

- The stability of oils reflects robust supply chains and low spot volatility, although gradual increases may be beginning to be felt in some countries and may soon become a practice globally.

- The war in the Middle East (which began on February 28, 2026) has caused significant disruptions in the global production of petroleum derivatives, including lubricants such as those in the table above, although the effects on lubricants are more indirect and later than on fuels.

Confirmed impacts on petroleum derivatives

- Fall in crude oil supply: Up to 8 million barrels per day less (IEA, March 2026), due to the closure of the Strait of Hormuz (20% of world oil), cuts in the Persian Gulf (Saudi Arabia, Iraq, etc.), and attacks on Iranian and regional refineries.

- Affected refineries: Shutdown of complexes in Iran, Qatar, and others, reducing capacity to produce base oils (raw material for lubricants). These impact derivatives such as gasoline, diesel, and lubricants.

- Lubricants specifically: what we can expect in the following months

-

- Price increase announced (not immediate shortages)

- Rising energy, transport, and raw material prices

- Lubricant refining process (vacuum distillation + hydrogenation) depends on stable crude

- Outages lead to delays of 1 to 3 months

Table of effects by product type

| Product | Production Drop | Main Reason | Impact on Lubricants |

|---|---|---|---|

| Crude Oil | ~8M bpd (March) | Hormuz + Gulf cutouts | Base for all products |

| Fuels | Onboard / Immediate | Refineries attacked, exports blocked | Lubricant transport |

| Base Oils | Medium / Late | Less crude for specialty distillation | Engine, Hydraulic, ISO 320 |

| Finished Lubricants | Low / Gradual | Additives + buffer stocks | Price increases between 10 to 20% |

Impact of the rise in oil prices on these economies

The rise in oil prices generates energy inflation, but the large economies can cushion through diversification and reserves.

- Importers (China, India, Japan, Germany, Brazil, UK, France): Cost increase by 10 to 20% in transport/industry.

- Exporters (Russia, Indonesia): They will generate extra profits and have plans to invest in local refining.

- USA: Minimal impact, less than 2%, refiners increase their profit margins.

Effect on demand and stock of lubricants

Although most countries have not yet seen a direct impact on end-user prices, the situation is not stable, and the impact is expected to materialize sooner or later.

| Lubricant | Demand | Current Stock (April 2026) | Impact Projection |

|---|---|---|---|

| Synthetic Engine Oil | HighCars — China / India / Japan | 3 to 6 monthsStable | ▲ 5 to 10% |

| Hydraulic OilISO 46 | Very HighMachinery — Germany / Brazil | 2 to 4 monthsPressure to keep stock | ▲ Up to 15% |

| ISO 320 Mineral Oil | HighHeavy Industry — China | 4 monthsDiversified impact | ▲ 10 to 20%Stable demand |

| ISO 320 Synthetic Oil | Medium-HighGears — Japan / USA | 3 monthsAdditives price increase | ▲ Up to 20%Critical stock |

Conclusions and recommendations

If you can negotiate the prices and purchase volumes of your plant and depend on the region where you are located, you can apply any of the following recommendations:

- The stock in Europe, the US, and China in the next 2 to 6 months is stable and there will probably not be a price increase, unless producers take advantage of this scenario; but if the conflict continues for more than months, there is a possible strangulation of the production chain with an immediate impact and increases in industrial oils starting in the summer.

- The 10 largest economies in the world and the surrounding countries are facing possible inflation, but they maintain a lubricant demand, as the industry is inelastic. This means that even though lubricant prices are likely to rise, the industry needs to buy what it needs.

- Secure short- to medium-term stocks with your lubricant supplier, or prioritize advanced purchases of the most-consumed products in your plant.

- Invest wisely in training for your maintenance personnel, in applications and tools that allow you to keep the lubricant in proper conditions and in lubricant analysis with which you ensure that when discarding oil it is because it no longer fulfills any of its main functions for which it has been designed and can have a negative impact on the lubricated component and the availability of the machine.